Regulation Name: GENIUS Act

Date Of Release: 31 March 2025

Region: United States

Agency: US Congress

The GENIUS Act: A New Chapter in US Stablecoin Regulation

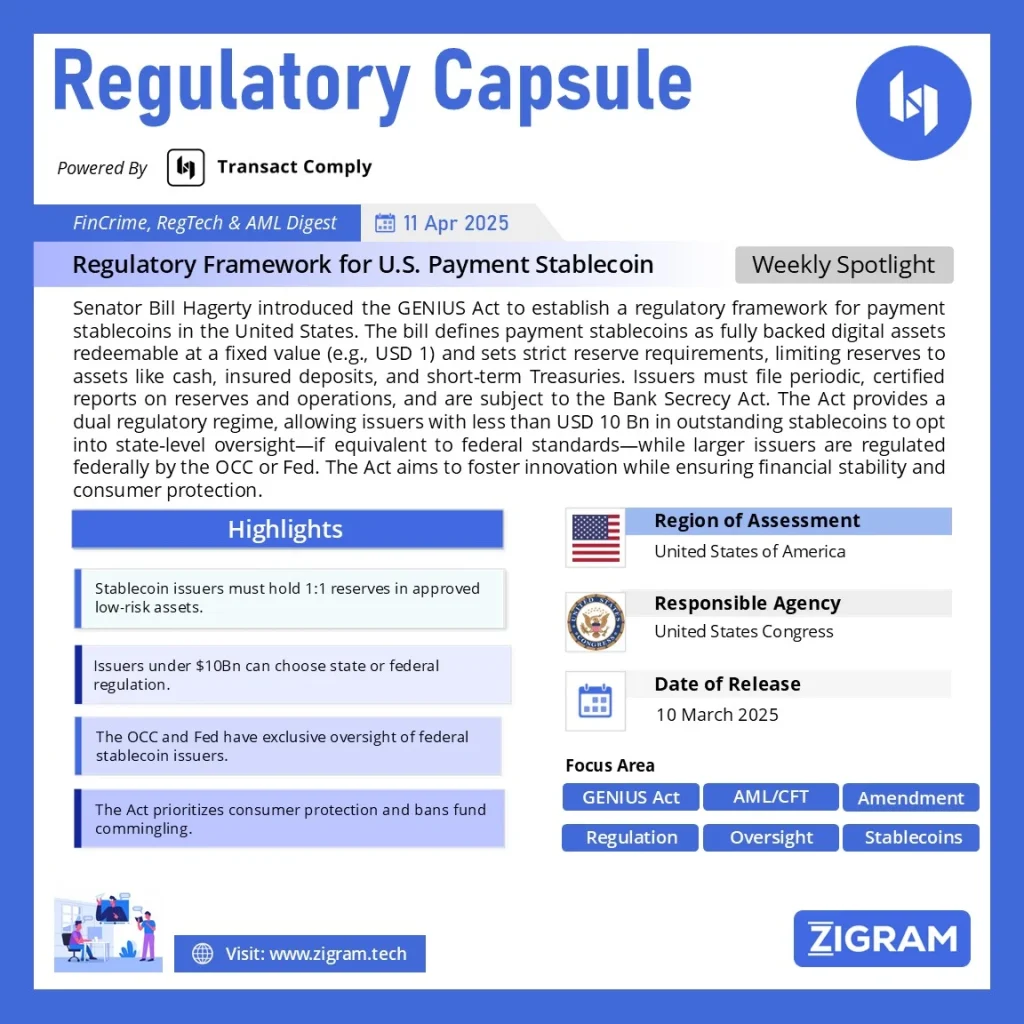

In early 2025, the United States took a significant step toward shaping the future of digital finance with the introduction of the Guiding and Establishing National Innovation for US Stablecoins Act—popularly known as the GENIUS Act. This bipartisan bill aims to establish a clear regulatory framework for payment stablecoins, seeking to ensure their secure use in everyday finance while maintaining the US dollar’s global dominance.

As the stablecoin market continues to grow, the GENIUS Act could serve as a model for regulatory clarity, similar to Europe’s Markets in Crypto-Assets (MiCA) regulation. With stablecoins like USDC and USDt becoming integral to digital payments, the legislation offers much-needed oversight, balancing innovation with financial security.

What Is the GENIUS Act?

Introduced on February 4, 2025, by Senators Bill Hagerty, Tim Scott, Kirsten Gillibrand, and Cynthia Lummis, the GENIUS Act was passed by the Senate Banking Committee on March 17, 2025, in a bipartisan 18–6 vote. Its objective is to create a secure environment for stablecoin usage, encourage innovation, and protect consumers—all while keeping the US dollar at the center of global financial activity.

The act introduces a dual oversight system, allowing stablecoin issuers to register under federal or state regulatory frameworks depending on their market capitalization. This flexible approach aims to promote innovation without compromising regulatory rigor.

Key Provisions of the GENIUS Act

🔹 Definition of a Payment Stablecoin

The act defines a payment stablecoin as a digital asset pegged to a fixed monetary value, fully backed on a 1:1 basis by US dollars or other high-quality liquid assets, and designed for use in payments and settlements.

🔹 Licensing and Oversight

Issuers with over $10 billion in market cap must register with federal regulators. Those below this threshold may opt for state-level regulation, provided the state’s rules meet federal standards. This dual-path approach aims to support smaller issuers while ensuring robust oversight.

🔹 Reserves and Audits

Issuers must:

• Maintain 1:1 reserves in liquid, high-quality assets (e.g., US Treasury securities).

• Segregate reserves from operational funds.

• Undergo monthly certifications and independent audits to ensure transparency and solvency.

🔹 AML and Consumer Protection

Stablecoin issuers are classified as financial institutions under the Bank Secrecy Act, mandating:

• Customer identification and due diligence

• Suspicious activity reporting

• Compliance with sanctions laws

In case of insolvency, stablecoin holders get priority over other creditors—offering significant consumer protection.

🔹 Clarity on Regulatory Jurisdiction

The bill explicitly excludes payment stablecoins from being classified as securities, commodities, or investment companies, helping eliminate confusion among regulators.

The Current Regulatory Landscape in the US

As of March 2025, stablecoin regulation in the US is fragmented. Agencies like the SEC and CFTC continue to vie for jurisdiction:

• The SEC treats many stablecoins like money market funds.

• The CFTC has classified some as commodities, fining Tether $41 million for misrepresenting its reserves.

Meanwhile, court decisions—such as the June 2024 ruling in favor of Binance—have underlined that 1:1 backed stablecoins like BUSD and USDC are not investment contracts, challenging SEC oversight.

This regulatory chaos underscores the need for a unified framework like the GENIUS Act.

Competing Bills in Congress

Several alternative bills propose different visions for stablecoin regulation:

• FIT 21 Act: Assigns oversight based on centralization—SEC for centralized, CFTC for decentralized stablecoins.

• Clarity for Payment Stablecoins Act: Offers a similar state/federal oversight model to GENIUS, while exempting stablecoins from securities laws.

• Maxine Waters’ Bill: Favors strict federal control, banning major tech firms like Amazon and Meta from issuing stablecoins.

• Lummis-Gillibrand Bill: Takes a balanced approach, stressing transparency, reserves, and consumer protections.

Potential Impact on the Industry

Opportunities for Stablecoin Issuers

Issuers like Circle (USDC) and Tether (USDt) may benefit from:

• Increased institutional adoption

• Greater consumer trust

• Regulatory legitimacy

However, they must ensure their reserves and operations align with the new requirements, potentially restructuring their portfolios.

Challenges for Smaller Issuers

Smaller or less transparent issuers might struggle to:

• Meet compliance obligations

• Undergo regular audits

• Maintain qualifying reserves

This could lead to market consolidation, reducing fragmentation and raising the bar for industry entry.

👥 Consumer and Investor Protection

The act enhances consumer safeguards:

• Priority claims in case of issuer bankruptcy

• Regular audits and disclosures

• AML/KYC compliance to prevent misuse

Criticism of the GENIUS Act

Despite its comprehensive vision, the bill has drawn criticism:

• Public Citizen warns it could enable high-risk crypto ventures and weaken safeguards.

• Critics argue that tech giants could exploit regulatory loopholes and blur lines between finance and commerce.

• The compliance burden might stifle innovation for smaller startups.

• Dual oversight might create inconsistencies across state and federal implementations.

Allegations of conflicts of interest—such as the Trump family’s reported interest in Binance.US and Commerce Secretary Howard Lutnick’s ties to Tether—have also sparked ethical concerns.

Conclusion: A Defining Moment for Stablecoin Regulation

The GENIUS Act marks a critical turning point in the regulation of digital finance. By combining clear definitions, stringent requirements, and flexible oversight, the act seeks to balance innovation, protection, and global competitiveness.

If successfully enacted, it could position the US as a global leader in stablecoin regulation, setting standards that influence markets worldwide. As stablecoins become increasingly central to the financial ecosystem, the GENIUS Act could prove to be the blueprint that brings order to a once-chaotic regulatory environment.

Read the full law here.

Read about the product: Transact Comply

Empower your organization with ZIGRAM’s integrated RegTech solutions – Book a Demo

- #AML

- #Compliance

- #GENIUSAct

- #Stablecoins