FCA Enforcement Data 2023-2024

The Financial Conduct Authority (FCA) has published its enforcement data for the fiscal year 2023/24, providing a detailed look at its efforts to protect consumers, maintain market integrity, and enforce regulatory standards. This report demonstrates the FCA’s increased use of data-driven strategies, early interventions, and robust enforcement actions to address regulatory breaches, financial misconduct, and systemic risks.

1. Harm Identification and Early Action

As a data-led regulator, the FCA has made significant strides in using advanced tools and platforms to detect potential harm early. The development of the Digital Unified Intelligence Environment has been instrumental in connecting data across multiple systems, enabling quicker identification of issues. This comprehensive data integration has allowed the FCA to spot trends, take early actions, and minimize harm before non-compliance or regulatory breaches occur.

A central component of the FCA’s harm prevention strategy is its Whistleblowing team, which receives disclosures from external whistleblowers. These disclosures are assessed and used to inform the FCA’s enforcement actions, enabling the agency to act swiftly on credible intelligence. Whistleblowing intelligence has proven to be a vital source of information, allowing the FCA to intervene before firms become non-compliant or cause harm to consumers.

The FCA’s Financial Promotions and Enforcement Taskforce (FPET) plays a pivotal role in enforcement activities, issuing warnings and alerts about firms engaging in regulated activities without proper authorization. This task force ensures that such firms are added to the FCA’s Warning List, which acts as a public notice of unauthorized firms operating in the financial sector. FPET also collaborates with other regulatory agencies, including the police, to refer potential investigations and ensure swift action against entities that pose risks to consumers and markets.

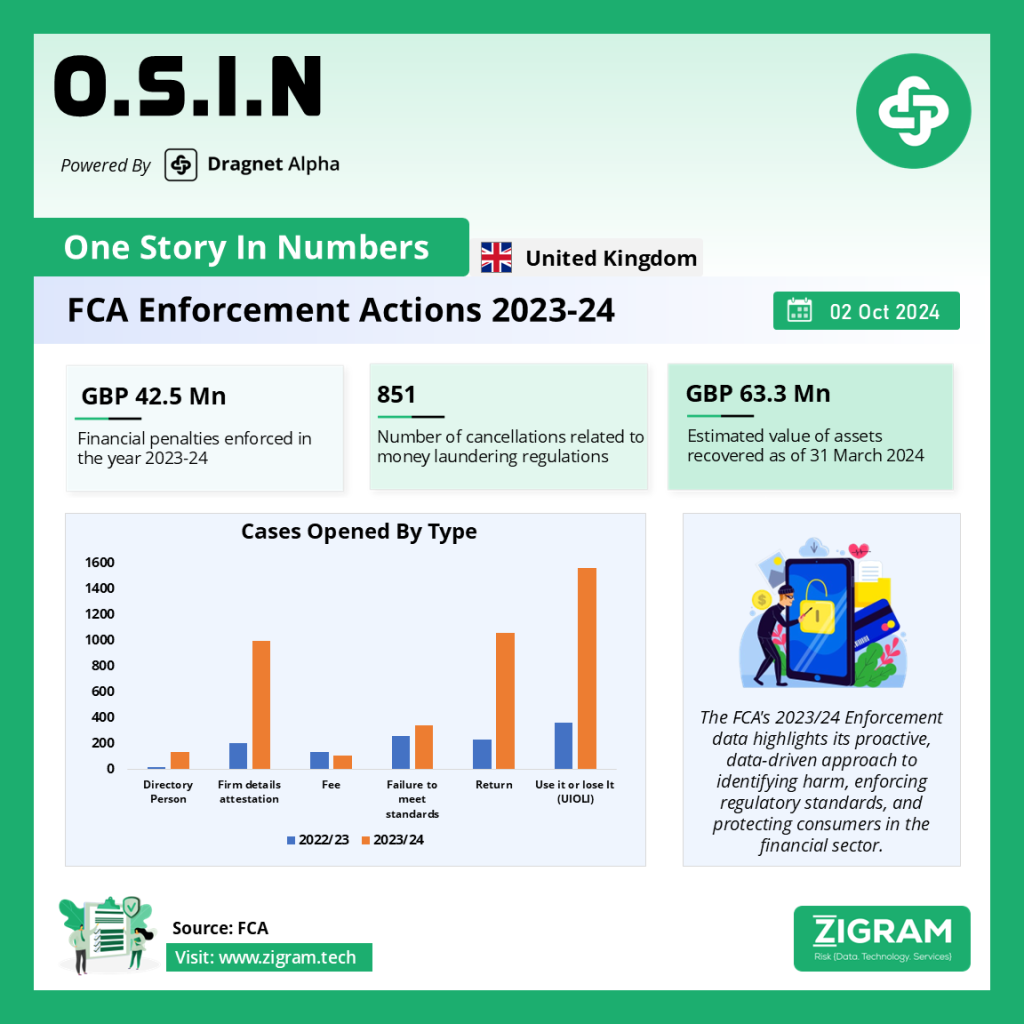

2. Meeting Threshold Conditions

The FCA monitors whether firms and individuals meet its minimum standards, known as Threshold Conditions, to maintain authorization in the financial services sector. Most of these cases are against firms, with issues ranging from failure to submit mandatory attestations to non-payment of regulatory fees.

Key findings for 2023/24 include:

– Cases Opened: Approximately 2,600 firms were subject to Threshold Condition cases, accounting for 98% of all cases, while 2% were against individuals.

– Case Types: Common issues included failure to submit Directory Persons Attestation, Firm Details Attestation, regulatory returns, or annual fees. Additionally, some firms were involved in “Use it or lose it” (UIOLI) cases, where they failed to conduct regulated activities associated with their permissions.

The data showed that the FCA opened a total of 4,260 cases in 2023/24, slightly up from 4,194 in 2022/23. A notable increase was seen in “Failure to meet standards” cases, highlighting the FCA’s focus on ensuring firms uphold regulatory requirements. This demonstrates the FCA’s heightened vigilance and readiness to act against firms not meeting its standards.

– Cases Closed: During 2023/24, the FCA closed 3,504 cases, with 97% related to firms and 3% involving individuals. This closure rate indicates the FCA’s efficiency in resolving cases and its commitment to maintaining market integrity.

The data reveals that while the FCA takes decisive action against firms that fail to meet standards, it also emphasizes rectifying issues to ensure compliance rather than immediately resorting to more severe measures like prohibitions or cancellations.

3. Intervention Actions

The Interventions team within the FCA plays a crucial role in addressing problem firms and preventing serious harm. By employing both formal and informal intervention tools, the team can swiftly engage with firms and individuals that pose a risk to consumers or market integrity. In 2023/24, the team advised on 268 cases, representing a 28% increase from 209 cases in the previous year. This uptick demonstrates the FCA’s proactive stance in identifying and addressing issues before they escalate.

Intervention actions included:

– Voluntary Outcomes: The FCA seeks to reach voluntary agreements with firms on the steps they must take to address concerns. In 2023/24, there were 102 voluntary outcomes compared to 82 in the previous year, indicating a preference for cooperative compliance.

– Own Initiative Outcomes: These include the use of formal powers to impose requirements, vary permissions, or take other actions against firms. The total number of own initiative actions increased from 22 in 2022/23 to 25 in 2023/24. Notably, the FCA increased its use of variations to Senior Management Function holder approvals, signaling greater scrutiny of individual accountability.

The data suggests that while the FCA prefers voluntary compliance, it is prepared to use its formal powers to address risks and protect consumers when necessary.

4. Enforcement Operations

The FCA’s enforcement operations target misconduct across wholesale, unauthorized, and retail sectors. In 2023/24, 188 enforcement operations were open, involving investigations into 341 individuals and 162 firms. These operations encompass various forms of financial misconduct, including market abuse, insider dealing, benchmark manipulation, and breaches of the Money Laundering Regulations.

The FCA categorizes its enforcement operations based on strategic priorities:

– Reducing and Preventing Financial Crime: Many investigations focus on detecting and preventing money laundering, fraud, and other financial crimes, ensuring that the financial sector remains free from criminal activity.

– Putting Consumers’ Needs First: Enforcement actions aim to protect consumers from harmful practices, such as the sale of unsuitable financial products or the mishandling of client funds.

– Strengthening the UK’s Position in Global Wholesale Markets: The FCA’s efforts to tackle market manipulation and insider dealing help maintain the integrity and competitiveness of the UK’s financial markets.

5. Asset Protection and Recovery

As of March 31, 2024, the FCA had 46 restraint or civil freezing orders in place, valued at over £60 million. These orders are designed to prevent the dissipation of assets linked to financial crime, ensuring they remain available for recovery or compensation. During the fiscal year, 9 new restraint or civil freezing orders were obtained, with an estimated value of £24.2 million.

These actions emphasize the FCA’s commitment to depriving criminals of the proceeds of their crimes and providing redress to victims.

6. Enforcement Outcomes

The enforcement outcomes for 2023/24 highlight the FCA’s increased activity and effectiveness in enforcing regulations:

– Final Notices: The FCA issued 316 Final Notices, a significant increase from 70 in the previous year, indicating intensified enforcement efforts.

– Financial Penalties: Total penalties imposed amounted to £42.59 million, with firms fined £38.36 million and individuals £4.23 million. While this represents a decrease from the previous year’s total, it suggests a more targeted approach to penalties based on the severity of breaches.

– Prohibitions and Cancellations: The number of prohibitions remained steady at 19, while cancellations surged from 195 to 851, reflecting the FCA’s readiness to take decisive action against non-compliant firms.

– Criminal Convictions: The FCA secured 11 criminal convictions in 2023/24, a substantial increase from 1 in the previous year, signaling its enhanced focus on prosecuting financial crimes.

7. Law and International Cooperation

In an increasingly interconnected financial world, the FCA’s investigations often span multiple jurisdictions. The FCA actively collaborates with international regulators and law enforcement agencies to tackle cross-border misconduct, particularly in areas such as online harm and new financial products. It remains the largest user of the International Organisation of Securities Commission’s (IOSCO) Multilateral Memorandum of Understanding (MMoU), facilitating information exchange and cooperation on enforcement actions across borders.

One of the FCA’s directors chairs IOSCO’s MMoU Monitoring Group, underscoring the FCA’s leadership in promoting global financial integrity and cooperation.

The FCA’s enforcement data for 2023/24 reflects a more proactive, data-driven, and collaborative approach to regulation and enforcement. By employing advanced analytical tools, fostering whistleblower intelligence, and engaging in international cooperation, the FCA is better equipped to identify harm, intervene early, and enforce compliance across the financial sector. The increase in enforcement operations, voluntary and formal interventions, and asset recovery measures demonstrates the FCA’s commitment to safeguarding consumers, maintaining market integrity, and reducing financial crime.

Read more about the FCA’s enforcement actions and strategies to stay informed on regulatory trends and the evolving financial landscape.

Please read about our product: Dragnet Alpha

Click here to book a free demo

- #FCAEnforcement

- #FinancialRegulation

- #MarketIntegrity

- #ConsumerProtection

- #FinancialCrime

- #AMLCompliance

- #Whistleblowing

- #RegulatoryCompliance

- #FinancialSector

- #DataDrivenRegulation

- #FinancialServices

- #MarketAbuse

- #AssetRecovery

- #FinancialPenalties

- #GlobalCooperation