The 2024 Payment Fraud Report by the European Central Bank (ECB) and the European Banking Authority (EBA) presents an in-depth analysis of payment fraud trends across various payment instruments. This article breaks down the key findings to provide a clear and comprehensive understanding of the data.

1. Absolute and Relative Levels of Fraud by Payment Instrument

The report provides detailed statistics on the absolute and relative levels of fraud across different types of payment instruments. Fraud rates for card payments and e-money transactions are significantly higher compared to other payment types. Specifically, for card payments, the fraud rate increased from 0.026% in the first half of 2022 to 0.031% in the first half of 2023. This increase was due to a decrease in overall card payments and an increase in the value of card fraud. E-money transactions showed a fraud rate of 0.022% in the first half of 2023, a decrease from previous periods.

2. Composition of Card Fraud

The composition of card fraud is divided into non-remote and remote transactions. A significant portion of fraud results from the theft of card details. Specifically, 61% of remote card fraud by value is due to the theft of card details. Lost or stolen cards account for 39% of non-remote card fraud by value. Fraud involving the manipulation of the payer is relatively low, contributing to 7% of remote card fraud by value.

3. Fraud Rates for SCA vs. Non-SCA Authenticated Transactions

The implementation of Strong Customer Authentication (SCA) has had a notable impact on fraud rates. Fraud rates for transactions authenticated via SCA are generally lower than those without SCA, particularly for transactions within the European Economic Area (EEA). However, for e-money payments, non-SCA transactions had lower fraud rates in terms of volume but higher in value compared to SCA transactions.

4. Composition of Losses by Liability Bearer and Payment Instrument

The report also delves into who bears the liability for fraud losses across different payment instruments. Most fraud losses for credit transfers, direct debits, and card payments are borne by Payment Service Providers (PSPs). For cash withdrawals and e-money, the losses are more evenly distributed between PSPs and Payment Service Users (PSUs).

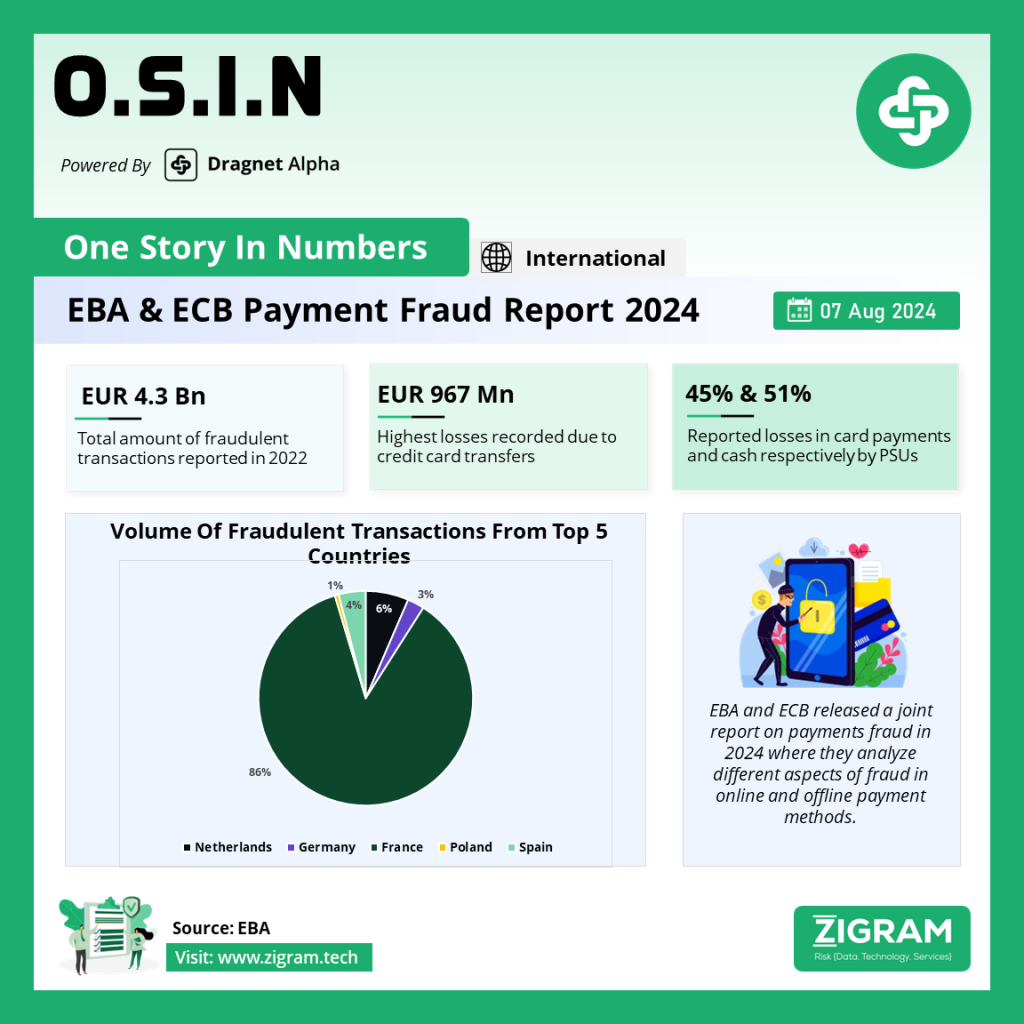

5. Geographical Dimension of Fraud

The geographical analysis shows that most payment transactions are domestic, yet a significant portion of card payment fraud is cross-border. Specifically, 71% of the value of card fraud in the first half of 2023 was related to cross-border transactions, highlighting the increased risk associated with such payments.

Key Takeaways

The 2024 Payment Fraud Report underscores the ongoing challenges in mitigating payment fraud across different instruments and regions. Key takeaways include:

– The rising fraud rates for card payments and the significant impact of cross-border transactions.

– The effectiveness of SCA in reducing fraud, particularly within the EEA.

– The need for continued vigilance and improved security measures to protect against evolving fraud tactics.

This comprehensive analysis highlights the critical areas where stakeholders must focus their efforts to combat payment fraud effectively.

Download the full report here.

Know more about the product: Dragnet Alpha

Click here to book a free demo.

- #PaymentFraud

- #ECB

- #EBA

- #FraudPrevention

- #SCA

- #CardFraud

- #EMoney

- #CrossBorderFraud

- #FinancialSecurity

- #Banking

- #Fintech

- #DigitalPayments

- #RiskManagement

- #FraudTrends

- #2024Report