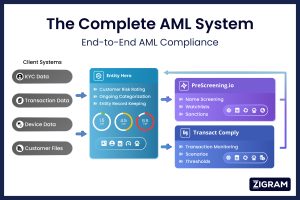

Payment processors are pivotal in the modern financial landscape, providing the technological infrastructure and services that enable businesses to accept and manage electronic payments. Their responsibilities include verifying and authorizing transactions, ensuring funds are transferred correctly, and managing the settlement process between merchants and financial institutions. By facilitating these transactions, payment processors help to maintain the fluidity and efficiency of the global financial system. Additionally, they offer value-added services such as fraud detection, chargeback management, and reporting and analytics, which are integral to the financial health of businesses.

India

India

India's AML regulations are governed by the Prevention of Money Laundering Act (PMLA). Payment processors are required to conduct KYC procedures, monitor transactions, and report suspicious activities to the Financial Intelligence Unit - India (FIU-IND). The regulatory framework in India is evolving, with increasing focus on digital payment platforms and fintech companies.

United States Of America

United States Of America

In the United States, AML regulations are governed primarily by the Bank Secrecy Act (BSA) and the USA PATRIOT Act. These laws mandate payment processors to implement comprehensive Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD) procedures, file Suspicious Activity Reports (SARs), and conduct regular sanctions screening. The Financial Crimes Enforcement Network (FinCEN) oversees compliance, emphasizing a risk-based approach to AML.

United Kingdom

United Kingdom

The UK's AML framework is largely shaped by the Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017, which align with the EU's AML Directives. The Financial Conduct Authority (FCA) enforces these regulations, requiring payment processors to conduct thorough CDD, monitor transactions for suspicious activity, and report any findings promptly. The UK's departure from the EU has led to independent enhancements of AML measures to address emerging risks.

European Union

European Union

The European Union's AML regulations are governed by the EU Anti-Money Laundering Directives (AMLD), with the 6th AMLD introducing tougher penalties and clearer definitions of money laundering offenses. Payment processors in the EU must adhere to strict CDD and EDD requirements, report suspicious transactions, and perform ongoing monitoring. The European Banking Authority (EBA) provides guidelines to ensure consistent implementation across member states.

Canada

Canada

Canada's AML regulations are overseen by the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC). Under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA), payment processors must implement CDD, report suspicious transactions, and maintain detailed records. Recent updates have strengthened requirements around virtual currencies and beneficial ownership transparency.

Singapore

Singapore

Singapore's AML regime is governed by the Monetary Authority of Singapore (MAS) under the Payment Services Act (PSA) and the Corruption, Drug Trafficking and Other Serious Crimes (Confiscation of Benefits) Act (CDSA). Payment processors must conduct CDD, file Suspicious Transaction Reports (STRs), and adhere to strict record-keeping requirements. Singapore's strategic location as a financial hub necessitates robust AML measures to mitigate risks associated with money laundering and terrorist financing.